Blockchain in Insurance – Opportunity or Threat

08/07/2016

Blockchain is a distributed ledger that is broadly discussed as a technology with huge innovation potential in all areas of financial services. To date, it is largely in the banking arena where blockchain use cases have been identified. However, the blockchain technology also offers potential use cases for insurers that include innovating insurance products and services for growth, increasing effectiveness in fraud detection and pricing, and reducing administrative cost. In these application areas insurers could address some of the main challenges they are facing today – such as limited growth in mature markets and cost reduction pressures.

Implementation of blockchain has a long-term horizon as it depends on network effects as well as on defining the regulatory conditions. Also, before initial implementation steps are taken, the benefits and limitations of the technology need to be fully understood.

Considering all of this, now is the best time for the insurance sector as a whole and for individual insurance players to further investigate the blockchain technology and its potential.

Quite a few voices are calling the emerging blockchain technology the greatest revolution since the advent of the Internet. In 2009, Bitcoin’s implementation of blockchain as the backbone for digital currency transactions was considered experimental and obscure. About five years later, financial institutions and central banks, along with VC started showing serious interest in applying blockchain beyond Bitcoin, and consortia such as R3 were set up.

At the same time, investments in blockchain-related start-ups across industries have quickly grown to more than USD 800 million in 2014/15. The McKinsey Panorama FinTech database currently registers over 200 blockchain-related solutions, of which about 20 provide use cases for insurers that go beyond payment transactions – either as specific applications or as base platforms. (1) Finally, even traditional insurance companies, such as AXA and Generali, have started to invest in blockchain applications and Allianz has just recently announced its successful pilot of a blockchain-based smart contract solution to automate catastrophe swap transactions.

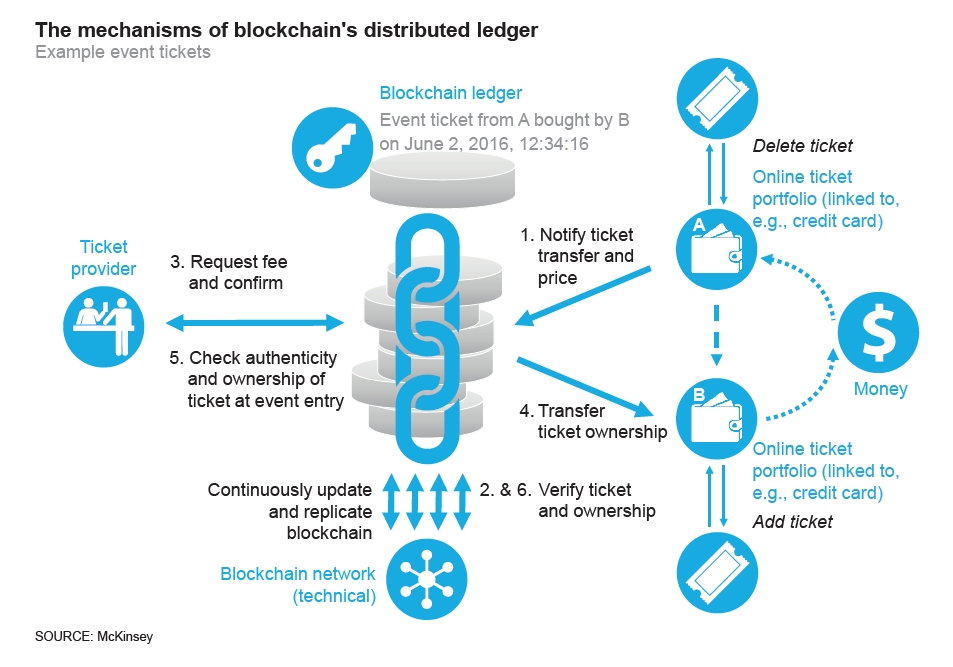

A blockchain is a distributed register to store static records and/or dynamic transaction data without central coordination by using a consensus-based mechanism to check the validity of transactions. As the Bitcoin backbone, blockchain was the first-ever solution to the double-spending problem that does not require a central administrator or clearing agent. (2) It is thus well suited for applications requiring transparency on records with a permanent time and date stamp, such as titles, document histories, and notary services.

While implementation spans different layers – from infrastructure to generic platforms to specific applications – a blockchain solution, without requiring central coordination, generally builds on a set of four characteristics:

– Decentralized validation

New data is packed into blocks that can only be added to the blockchain after consensus is reached on the validity of the action, e.g., a ticket seller is the legitimate owner of a ticket – see illustration below. This allows participants to place trust in their transactions even in the absence of a central authority, thus enabling disintermediation. Validation may require heavy computing power, which is provided

by the processors in the computers of participants in the blockchain network, making it difficult for hackers to simulate and manipulate the validation. Alternative approaches to validation can be implemented, depending on the implementation’s targeted use case(s), e.g., to make it more scalable.

– Redundancy

The blockchain is continuously replicated on all or at least a group of nodes in the network. As a result, no single point of failure exists.

– Immutable storage

Each stored block is linked to its previous block in the chain, making it almost impossible for hackers to subsequently change blocks, as they would have to manipulate any succeeding block plus the majority of their replications. Furthermore, data is registered in the blockchain by creating a digital fingerprint using hash functions with a date and time stamp. Any attempt to change data will be apparent, because the new digital fingerprint will not match the old one. Combined with the chaining of blocks, the stored data becomes immutable, and full transparency on the history of transactions is reached.

– Encryption

Digital signatures based on pairs of cryptographic private and public keys put network participants in a position to authenticate which participant initiated a transaction, owns an asset, signed a (smart) contract, or registered data in the blockchain.

With these characteristics, in general, blockchains can be used as a system of static record keeping (e.g., for land titles), and as a dynamic registry for the exchange of assets and payments as well as for the verification of dynamic information (e.g., tickets).

They are also a platform for smart contracts, which are small programs running on a blockchain and initiating certain actions when predefined conditions are met.

2. Blockchain’s potential use cases for the insurance industry

In the banking industry, several blockchain use cases are currently being implemented, ranging from customer-facing payment technology to trading and exchange services. (3) While the insurance industry (in terms of technology adoption) lags behind banking, it is nevertheless uniquely positioned to benefit from blockchain technology. Blockchain can address the competitive challenges many incumbents face, including poor customer engagement, limited growth in mature markets, and the trends of digitization. In the following, we outline the most promising insurance-related use cases in three categories: enabling growth, increasing effectiveness, and reducing cost by automating key processes.

Innovate products and services for growth

We see three ways in which blockchain can facilitate growth for insurers: improving customer engagement, enabling cost-efficient product offerings for emerging markets, and enabling the development of insurance products related to the Internet of Things. Fundamental to the potential that blockchain offers in these areas is its usage as a distributed and reliable platform for customer-controlled personal data, peer-to-peer (P2P) insurances, and smart contracts.

– Customer engagement

An important lever for improving customer engagement through blockchain lies in the area of personal data. Customers’ fears about losing control of personal data as soon as it is handed over to a company and their frustration with the need to repeat data entry processes can be addressed by a customer-controlled blockchain for identity verification (see KYC use case) or medical/health data.

Personal data does not need to be stored on the blockchain; it remains on the user’s personal device. Only its verification, e.g., through a doctor, and related transactions (e.g., an examination that has taken place on a certain date) are registered in the blockchain. Here, scale is key to reaping the benefits of blockchain as it requires a sufficient number of parties involved to reuse the verified data.

—————-

“Speed up and simplify the onboarding of new customers” – the KYC use case Start-ups like Tradle are working on blockchain solutions for know-your-customer (KYC) data. With KYC, the customer grants a company access to identity data when necessary for a contract closure. Once the KYC profile is verified, a customer can forward the verified identity data to other companies for different contracts with the same tool, avoiding the need to repeat the full identification and verification process, thus speeding up and increasing efficiency in the onboarding of new customers.

—————-

Blockchain can also improve customer engagement by providing a greater degree of transparency and perceived fairness of tariffs and claims handling. For example, the start-up InsureETH demonstrated a P2P flight insurance policy built on blockchain with smart contracts. These smart contracts initiate payouts for insured flight tickets when cancellations or delays are reported from verified flight data sources (via so called “oracles” for making external sources usable for smart contracts in the blockchain).

While P2P insurance as a business model is already being offered using standard technology, blockchain makes it even more transparent and trustworthy for consumers as no central authority controls its operation. For the provider, it is a tool to widely automate P2P insurance operations.

Whether they are used as part of P2P insurance or not, smart contracts on top of a blockchain offer several benefits: they enable automation of claims handling, they are a reliable and transparent payout mechanism for the customer, and they can be used to enforce contract-specific rules. For example, in the case of a car accident, a smart contract can ensure that the claim is only paid out if the car is repaired in a garage preferred and predefined by the insurer. Although such programs could also be implemented without blockchain, a blockchain-based smart contract platform could provide unique benefits. Not only does it deliver an increased degree of transparency and credibility for customers due to decentralization as well as automation of reconciliation and verification of transactions, but it also provides substantial network effects – either in the case of P2P insurances or when several parties are using it that would not be able or willing to do this with a centralized platform.

—————

“Automate underwriting and claims handling” – the use case of smart contracts Dynamis is one of the blockchain start-ups innovating in the area of smart contracts for insurance products. The company is developing a P2P supplemental unemployment insurance and uses social network profile data for verification of the employers’ status. In this case, the smart contracts are automating the underwriting of policies and claims handling – combined with approvals/verifications from other policyholders, who serve the role of evaluators.

—————

– Emerging markets

In emerging markets P2P blockchains with smart contracts could be applied to micro-insurances to offer them at low handling costs, if underwriting and claims handling can be automated based on defined rules and the availability of reliable data sources. Payouts to insured farmers, for example, might be triggered when drought conditions are reported by verified climate/weather databases.

– Internet of Things (IoT)

Looking forward to the IoT, cars, electronic devices or home appliances can have their own insurance policies registered and administered by smart contracts in a blockchain network, automatically detecting damage first and then triggering the repair process, as well as claims and payments.

Increase effectiveness in fraud detection and pricing

An estimated 5 to 10 percent of all claims are fraudulent. According to the FBI, this costs US non-health insurers more than USD 40 billion per year. To more effectively detect identity fraud, falsified injury or damage reports, etc., blockchain can be used as a cross-industry, distributed registry with external and customer data to:

– Validate authenticity, ownership, and provenance of goods as well as authenticity of documents (e.g., medical reports)

– Check for police theft reports/claims history as well as a person’s verified identity and detect patterns of fraudulent behavior related to a specific identity

– Prove date and time of policy issuance or purchase of a product/asset

– Confirm subsequent ownership and location changes.

However, to achieve blockchain-specific benefits from these applications beyond what is possible with traditional database solutions and existing forms of cooperation – e.g., via industry associations –, intensive cooperation between insurers, manufacturers, customers, and other parties is necessary. This is yet another example of an ecosystem growing beyond the traditional insurance industry as seen in the connected car scenario. (4)

——————–

“Make fraud detection easier” – the use case of product authentication

One start-up in the fraud detection area is Blockverify for goods such as electronics, pharmaceuticals, and luxury items. Its solution allows users to check for counterfeit products, diverted or stolen goods, and fraudulent transactions. It works by labeling products and then storing the history and supply chain in the blockchain. A similar, well-known application is Everledger, which is used for the verification of diamonds and related transactions.

——————–

Related to the IoT developments and also relevant for sharing economies (e.g., Uber, Airbnb) are usage- or sensor-based insurances, which have already become a market with millions of customers, especially for usage-based car insurance, and continue to grow. Here, blockchain can be used for applications that register a policyholder’s usage or health data, for example, and let smart contracts calculate/update the tariffs. Again, a key advantage could be achieved if access control to such sensitive data can remain with the customer while data is verifiable and (after approval by the customer) reusable for other parties.

Reduce administrative cost

Blockchain may reduce administrative/operations cost through automated verification of policyholder identity and contract validity, auditable registration of claims and data from third parties (e.g., encrypted transaction of patient data between doctor and injured party accessible by insurer to verify payment), and payouts for claims via a blockchain-based payments infrastructure or smart contracts. Giving reinsurers, for example, controlled access to claims and claims histories registered on the blockchain improves transparency for the reinsurer in an automated and, at the same time, auditable way.

3. Conditions and limitations in applying blockchain

The implementation of blockchain should be considered under certain conditions. If the transactions currently involve multiple parties and require not only the assurance of an intermediary, but also a precise and immutable record of the date and time, blockchain offers a disintermediation solution. Blockchain can be useful as well in situations where the parties involved in transactions have potentially competing incentives, retroactive manipulation of data is a risk, or multiple uses of the same asset are very likely and no central trusted authority is available/wanted.

Conversely, there are conditions under which blockchain is likely not an appropriate solution. If transactions involve only a limited number of parties – or do not require an intermediary – or if a well-established, trusted intermediary already exists, insurance players may be well advised to continue working under their current transaction models.

Before taking concrete action, companies need to become familiar with the limitations of this technology in terms of scalability, security, and standardization.

– Scalability

Because of the consensus-based validation mechanisms and the continuous replications, as well as the ever-growing amount of stored data (set to be immutable), the scalability of a blockchain system is a challenge. Even if there are newer implementations of blockchain that have fewer performance restrictions, high-speed/high-volume transactions, real-time data capture, and storage of large volumes data are not the

intended domains of blockchain.

– Security

Recent incidents have shown that in a blockchain ecosystem new types of attacks are coming to existence. These are far less understood and, therefore, less mitigated as those occurring in conventional database architectures.

– Standardization

To realize sustainable benefits from an open or, at least to some extent, shared and distributed system, standards are absolutely critical. A lack of standards and of proven, successfully applied reference implementations are indications that the technology is still in its infancy. Thus, the risk of implementing inefficient solutions and the need for pre-implementation efforts to define and establish industry standards are high, and investment decisions need to be taken very carefully.

4. Outlook on next steps for the insurance industry and individual insurance companies

Blockchain is a technology ready for exploration by insurers. But its exploitation is still a long way off. This is because blockchain is functioning as a distributed system and, thus, its value mostly depends on collaboration with competitors, suppliers, or others.

Blockchain is an IT investment with a perspective of presumably five years until full realization of benefits. In application areas that do not strongly rely on blockchain’s distributed mechanisms, alternative solutions can provide similar benefits much sooner. On the other hand, while proof is outstanding, blockchain promises unique potential for insurers to efficiently serve emerging markets with P2P micro-insurances, develop products for the IoT market, or reliably share data from and with other parties for improvements in, for example, fraud detection or automation of claims handling.

For the industry as a whole, this means starting to work with consortia, technology experts and start-ups, regulators, and other market participants to identify the challenges around blockchain’s open and decentralized nature. Among these challenges are technology limitations as well as market, legal/regulatory (who is regulated in the absence of an intermediary or in cross-border solutions?), and operational requirements regarding, for example, data protection and standardization.

Individual insurance companies should start with a holistic understanding of customer engagement needs and their own pain points to assess where the most promising blockchain use cases exist. As an innovative technology, blockchain presents a threat for incumbents in the form of innovative business models and/or cost advantages. But, there is a range of options to counteract this threat by adopting the way of working of start-ups, partnering with, or acquiring them. Key to shaping the future of the blockchain insurance ecosystem is getting involved in partnerships and industry activities early on.

Blockchain is a digitization technology that could be of strategic interest for insurers. The biggest challenges to its industry-wide implementation are facilitating collaboration between market participants and technology leaders, succeeding in the operational transformation, and shaping a stimulating regulatory environment. Laying the foundation to address these challenges today will put insurance companies in a position to have at-scale blockchain use cases and profit from the technology’s benefits in about five years from now.

Authors and experts:

Johannes-Tobias Lorenz, Senior Partner, Düsseldorf

Björn Münstermann, Partner, Munich

Matt Higginson, Associate Partner, New York

Peter Braad Olesen, Associate Partner, Copenhagen

Nina Bohlken, Engagement Manager, Cologne

Valentino Ricciardi, Knowledge Specialist, Milan

(1) We introduce some of the blockchain insurance start-up companies in Section 2.

(2) As described by the Bitcoin inventor Satoshi Nakamoto (a pseudonym) in “Bitcoin: A peer-to-peer electronic cash system.” 2008, https://bitcoin.org/bitcoin.pdf.

(3) See also: Tolga Oguz, Roger Rudisuli, Matt Higginson, Jeff Penney, “Beyond the Hype: Blockchains in Capital Markets.” December 2015, McKinsey.com.

(4) Markus Löffler, Christopher Mokwa, Björn Münstermann, Johannes Wojciak, “Shifting gears: Insurers adjust for connected-car ecosystems.” May 2016, McKinsey.com.

Participez aux prochaines conférences Blockchain éditées par Finyear Group :

Blockchain Vision #5 + Blockchain Pitch Day #2 (20 septembre 2016)

Blockchain Hackathon #1 (fin 2016).

Les médias du groupe Finyear

Le quotidien Finyear :

– Finyear Quotidien

La newsletter quotidienne :

– Finyear Newsletter

Recevez chaque matin par mail la newsletter Finyear, une sélection quotidienne des meilleures infos et expertises en Finance innovation, Blockchain révolution & Digital transformation.

Les 6 lettres mensuelles digitales :

– Le Directeur Financier

– Le Trésorier

– Le Credit Manager

– The Chief FinTech Officer

– The Chief Blockchain Officer

– The Chief Digital Officer

Le magazine trimestriel digital :

– Finyear Magazine

Un seul formulaire d’abonnement pour recevoir un avis de publication pour une ou plusieurs lettres